Free IL

Free IL

This insightful article from SteadyOptions, titled “IV Crush Explained – How Implied Volatility Crush Works,” provides a clear and practical explanation of one of the most misunderstood phenomena in options trading: implied volatility (IV) crush. Perfect for beginner and intermediate options traders, the article demystifies why option prices often plummet after major events—like earnings reports—even when the stock moves in the anticipated direction.

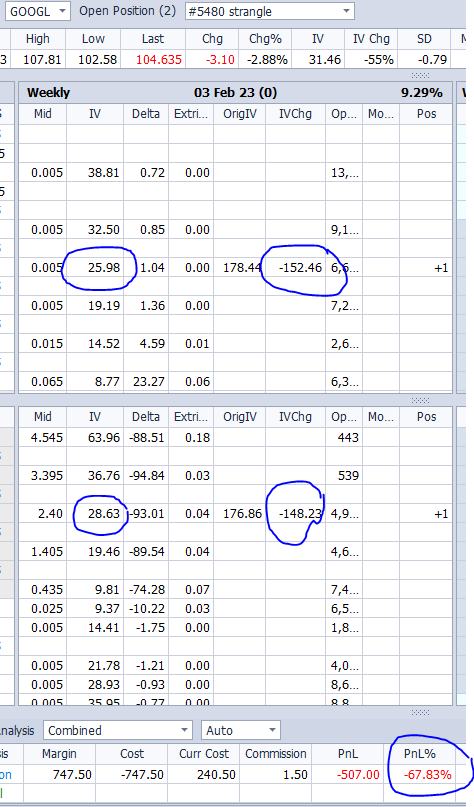

The article begins by defining implied volatility as the market’s forecast of a stock’s potential movement. It then explains that prior to scheduled events, IV often spikes as uncertainty grows. Once the event occurs and the uncertainty is resolved, IV drops rapidly—a phenomenon known as IV crush—causing a sharp decline in the premiums of both call and put options.

Through real-world examples and option chain illustrations, the article shows how IV crush can negatively impact long option positions, even when traders correctly predict price direction. It also discusses how traders can use strategies like credit spreads, calendars, and iron condors to benefit from IV crush instead. Overall, the article is an essential read for anyone looking to understand volatility dynamics and adjust their strategies accordingly to avoid costly surprises.